What is a Budget?

A budget is a plan on how you spend your money. It includes income, or the amount of money you have available each month. It also includes expenses, or what is spent each month.

A budget helps you decide how to spend your money and how to change spending if you need to. A budget is important for everyone, especially when:

- we may be behind in paying bills, such as rent or utilities, or paying off debt;

- we want to make the most of our money but are not clear how much we are spending on what kinds of things; or

- we want to plan for certain purchases, unexpected bills or emergencies.

Making a Budget

The first step of making a budget is to keep track of the money received and where that money comes from. This includes all money from a job and federal and provincial benefit programs (e.g. Employment Insurance, Canada Child Benefit, Goods and Services Tax Rebate Program, etc.).

Second, keep track of monthly expenses and list them. This includes rent, utilities, groceries and other regular payments you need to make.

Subtract these expenses from your income.

If expenses are greater than your income, you may need to:

- find areas to cut back or reduce spending; or

- look for ways to increase your income.

If your income is more than your expenses, you should try to save some money for unexpected bills or emergencies.

Example of a budget

| Your Income |

Your Expenses |

| Earned Income |

$1,600 |

Rent |

$1,100 |

| Canada Child Benefit |

$540 |

Utilities |

$250 |

| Total Income |

$2,140 |

Groceries |

$575 |

| |

Insurance |

$56 |

| |

Transit |

$75 |

| |

Total Expenses |

$2,056 |

Total Remaining Budget

|

|

$84 |

Needs and Wants

If you think you need to change your spending habits, it is important to think about what you "need" and what you "want."

Some "needs" include:

- housing and food costs;

- things for work, such as travel or clothing;

- heat, water and power; and

- costs related to having children.

Some "wants" include:

- entertainment costs;

- eating out; and

- electronics we don't really need.

Understanding needs and wants will help you to manage within your monthly budget.

How to create a budget summary that outlines your income and expenses

Download the Budget Summary Worksheet and enter your income and expenses. The income section includes spaces to enter all the types of income you may get. Be sure to enter your net income (income after all deductions have been made). The expense section is divided into four categories. Not all may apply to you, but fill out what you know.

At the bottom of the worksheet, your net income is the total of all your income, and your net expenses is the total of all your expenses. In the "net gain/loss" area:

- If your total is not in brackets, your income is higher than your expenses. You may want to think of ways to save for the future.

- If your total is in brackets, your expenses are higher than your income. You may need to think of ways to reduce or cut some of your expenses. The Wants and Needs Calculator may help with this.

Tips for Increasing Income

- Completing your income taxes each year makes sure you get all federal and provincial benefits you are eligible for. This includes Goods and Services Tax Credit, Canada Child Benefit, Canada Pension Plan, etc.

- Continue to look for improved employment opportunities to increase your monthly income. Consider steps to get a better job, including career counselling, training or education programs. For more information, please visit Labour Market Services.

Tips for Lowering Costs

- Budget for current expenses and any debt or outstanding payments you need to make. If you are behind on a utility, for example, try to pay your current amount plus a portion of what you owe. Contact your utility provider to make sure they are aware you have a plan and discuss options with them.

- Cut down on the biggest expenses when you can. Cut back on utility use by turning off lights, lowering your thermostat overnight or when not at home. Contact your utility company to see what tips they can offer, or visit these websites for tips:

- Be very selective when looking for new accommodations. Understand the total housing cost (i.e. rent and utility amounts). For more information on social housing, please visit the Saskatchewan Housing Corporation.

- Cut back on cable, internet and cellphone plans. Look for apps that offer free messaging and long-distance calling. Contact your service provider and ask how payments can be lowered.

- Reduce food costs by purchasing in bulk. Use grocery stores that have lower mark ups and use coupons to save money.

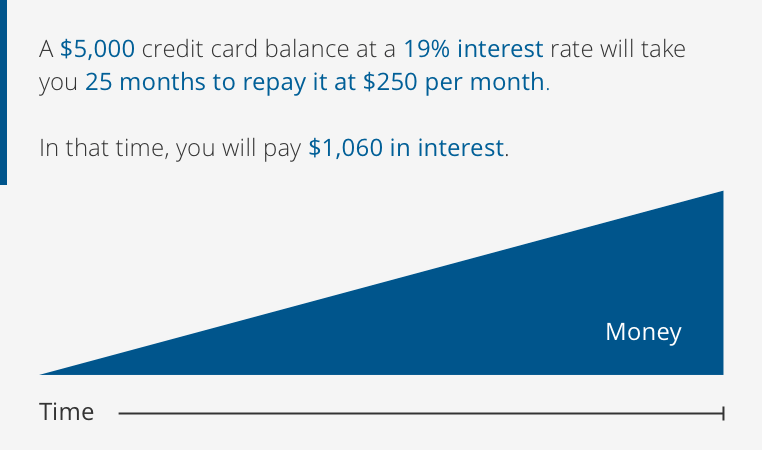

- Determine the amount you can spend on groceries. Paying with cash can help to ensure you do not overspend. Credit cards are convenient, but they have high interest rates and, if not paid on time, will cause greater debt.

How to reduce your expenses

Use the Wants and Needs Calculator to help think of ways to reduce or cut expenses.

To use the calculator, enter the cost of an item in the 'cost' column, and the number of times per month you spend this amount in the 'frequency' column. The result is how much you spend a month on a particular item. For example, if your 'cost' for eating out is $15, and the 'frequency' is 15 times a month, the monthly cost is $225. If you reduce eating out to 5 times a month, your monthly cost is $75. Cutting down on the number of times you eat out each month saves you $150.